Abi Malin

Article

The best fintech products of the next decade won't look like fintech at all.

After years of unbundling traditional banking services into standalone apps — digital wallets, neobanks, investment platforms — we're watching a fundamental shift in how financial services reach consumers and businesses. The winners of the next decade won't build better standalone fintech products. They'll make financial services invisible by embedding them directly into the software consumers already use, powered by AI that makes intelligent decisions on their behalf.

This isn't an incremental improvement. It's a transformation from financial services as destinations to financial services as infrastructure.

"The winners of the next decade won't build better standalone fintech products. They'll make financial services invisible."

The Convergence Creating Opportunity

Three major trends are driving it:

-

Embedded finance infrastructure has matured.

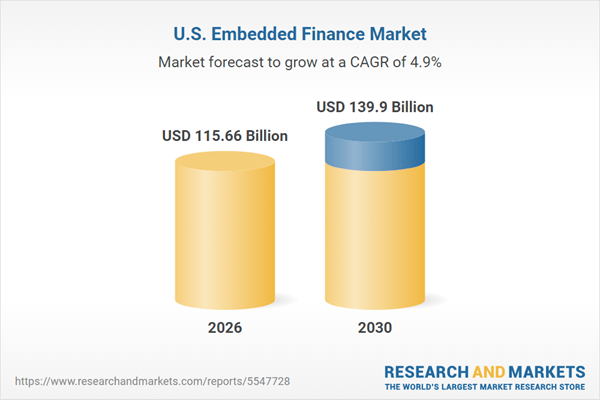

Banking-as-a-service (BaaS) platforms like Stripe Treasury, Unit, and Synctera have made it dramatically easier for non-financial companies to offer financial products. What once required years of regulatory work and millions in capital can now be launched in months through API integrations.The market has responded accordingly. According to Research and Markets, the U.S. embedded finance market reached $115.66 billion in 2025 and is projected to reach $139.90 billion by 2030, growing at a 4.9% CAGR.

-

AI has reached practical utility for financial decisions.

Unlike earlier waves of "AI-powered" fintech that were mostly rules-based automation with fancy marketing, today's large language models and machine learning systems can genuinely improve financial outcomes. They can analyze spending patterns, predict cash flow needs, optimize payment timing, and personalize financial products at scale.

As Bain Capital's Matt Harris notes: "AI companies are not competing with software budgets; they are competing against hard labor costs." This is particularly true in fintech, where AI is automating human-intensive functions like underwriting, compliance, and customer service. -

Consumer expectations have fundamentally shifted.

People no longer want to context-switch to manage their finances. They want financial services working seamlessly within their existing workflows — whether that's getting paid instantly through a gig platform, accessing working capital through their e-commerce dashboard, or getting financing offers at checkout.

The data supports this: Toast (NYSE: TOST), which embeds payments, lending, and financial management into restaurant software, now serves over 156,000 restaurants and trades at a $16+ billion market cap. Restaurants don't use Toast because it's the best payment processor—they use it because financial services are seamlessly integrated into the software that runs their business.

Why Embedded Finance + AI Changes Everything

Embedded finance alone has been powerful, but largely transactional. AI transforms it from a convenience into a competitive advantage by adding intelligence to every financial interaction.

Consider the evolution of business lending:

-

Traditional model: Small business applies for loan at bank, waits weeks for underwriting, gets generic terms

-

Embedded finance (V.10): E-commerce platform offers instant working capital based on sales data

-

AI-powered embedded finance: Platform continuously monitors business performance, proactively offers optimized financing before cash flow issues arise, automatically adjusts terms based on real-time risk assessment

Shopify Capital is already operating in that third phase, using merchant sales data and AI to underwrite loans instantly — deploying more than $2.8 billion in the first nine months of 2025. And they're still in early innings. The AI sophistication and decision automation will only deepen from here.

The Golden Zone: Where to Invest

Based on our analysis of the embedded finance landscape, the most compelling investment opportunities sit at the intersection of deep platform integration and sophisticated AI capabilities. We call this the "golden zone" — companies that aren't just connecting financial services via APIs, but embedding intelligent financial decision-making directly into core workflows.

Here's what distinguishes golden zone companies:

Deep Integration: Financial services feel native to the host platform, not bolted on. Users complete 95%+ of financial actions without leaving the primary application. Think Stripe's embedded payment and financing products within e-commerce platforms, or Ramp's expense management embedded in accounting software.

AI-Native Architecture: Intelligence is core to the product, not a feature. The system learns from user behavior, predicts needs, and makes autonomous decisions. For example, Brex uses AI to automatically categorize transactions, flag anomalies, and optimize credit utilization — reducing finance team workloads significantly.

Data Network Effects: The more the platform is used, the better the AI decisions become, creating exponential improvements in value delivery. This is why Treasury Prime's embedded banking infrastructure becomes stickier over time — their models improve with every transaction processed.

What We're Watching: Key Metrics for Success

When evaluating AI-powered embedded finance companies, we focus on metrics that demonstrate both the depth of integration and the value of AI intelligence:

Core Embedded Finance Metrics

Attachment Rate: What percentage of the host platform's users adopt the financial product?

Low attachment rates signal poor product-market fit or shallow integration. According to BCG and Adyen (AMS: ADYEN) research on embedded finance in North America, top-performing platforms generate over 50% of revenues from embedded payments and finance, with embedded solutions showing 2.5x lower customer attrition than standalone alternatives. While benchmarks vary by vertical and product type, the principle is clear: higher attachment rates indicate that the financial service has become integral to the platform's core value proposition.

Revenue Share & Take Rate: What percentage of transaction volume does the company capture, and how is it split between provider and platform?

Research shows that successful platforms typically capture take rates of 0.5 - 2% on transaction volumes, with revenue splits varying based on risk allocation and value contribution between the platform and financial infrastructure provider.

Integration Depth: How seamlessly integrated is the product?

We measure API touchpoints and how often users complete actions without external redirects. Deep integration - where the financial service feels native to the platform experience - creates defensibility that shallow, bolt-on integrations can't match.

AI-Specific Value Metrics

AI-Driven Conversion Lift: Can the company prove the AI meaningfully outperforms non-AI alternatives? According to a 2025 academic study in the Global Journal of Engineering and Technology Advances, AI-powered systems in financial services achieved a 32% increase in approval rates while maintaining acceptable risk parameters, with some implementations showing improvement rates as high as 40%. A/B testing should demonstrate measurable improvements in approval rates, customer adoption, or revenue per user to demonstrate genuine AI advantage.

Automated Decision Accuracy: For AI-driven decision systems, the company should track false positive/negative rates and the percentage of decisions requiring human review.

The best systems demonstrate high accuracy with minimal manual intervention and show continuous improvement over time as models learn from new data.

Personalization Impact: Can the company quantify the value of AI-driven personalization?

We look for measurable improvements in engagement, cross-sell success, and customer satisfaction alongside revenue gains.

Business Model Health

Multi-Product Expansion: How quickly do customers adopt additional embedded financial products?

Strong companies track product attach rates to measure the effectiveness of their land-and-expand strategies. Best in-class companies achieve net revenue retention above 120%, indicating successful expansion revenue from existing customers through cross-sells and upsells.

Platform Dependency Risk: What's the revenue concentration across host platforms?

For embedded finance companies, platforms are customers, making standard customer concentration risk frameworks directly applicable. In early stages, companies with concentration of 70%+ from the top five platforms signals high risk. As companies scale and mature, we expect diversification to increase and concentration to decrease.

Unit Economics with AI Costs: After factoring in ML compute, data, and model maintenance costs, what are the true unit economics?

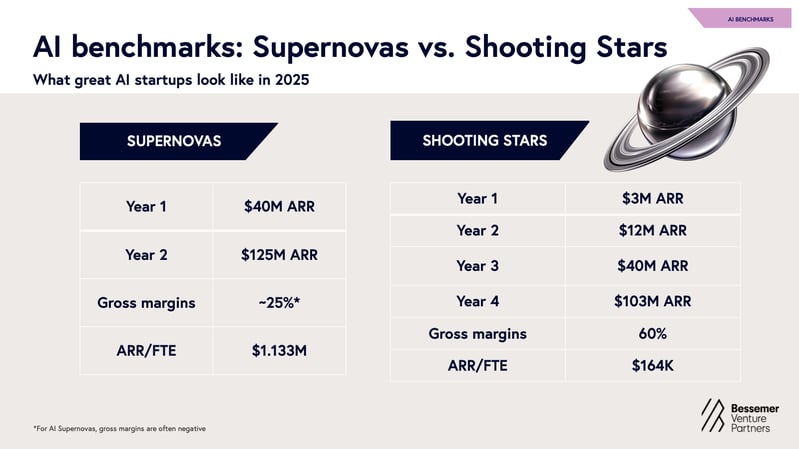

While traditional SaaS companies achieve gross margins of 70-85%, according to Bessemer Venture Partners “The State of AI 2025” report, “AI supernovas” (meaning AI startups reaching $40M in year 1) exhibited 25% gross margins and “AI shooting stars” (meaning AI startups reaching $3M ARR in year 1) exhibited 60% gross margins. To make the margins work for an AI-company at scale, a startup should use intelligent model routing, implement usage-based pricing, and add value beyond just the AI-compute aspect to drive improving unit economics over time.

Red Flags That Make Us Pass

Even compelling markets have bad investments. Here's what makes us walk away from AI-powered embedded finance deals:

-

High AI infrastructure costs that don't improve with scale. If ML compute costs remain a percentage of gross revenue at scale, the unit economics won't work. The best companies see AI costs decline as a percentage of revenue as they grow.

-

Overdependence on a single host platform. Heavy platform concentration means a startup is one API change away from disaster. We need to see a clear path to platform diversification.

-

Attachment rates below 10%. If less than 10% of the host platform's users adopt your financial product, you haven't achieved product-market fit within the embedded context. Great standalone products can still fail as embedded offerings.

-

Low model accuracy or excessive manual review. As the AI adoption surges, corporate clients have budgets to test and trial various AI tools. However, in the longer term, I believe those budgets will rationalize. I expect that end users will need to have measurable efficiency gains from the product.

-

No regulatory strategy. AI makes financial decisions faster and often better, but regulators want to know how, why, and whether those decisions are fair. Companies without a clear strategy for all three are carrying risks that can kill them.

The Market Opportunity Ahead

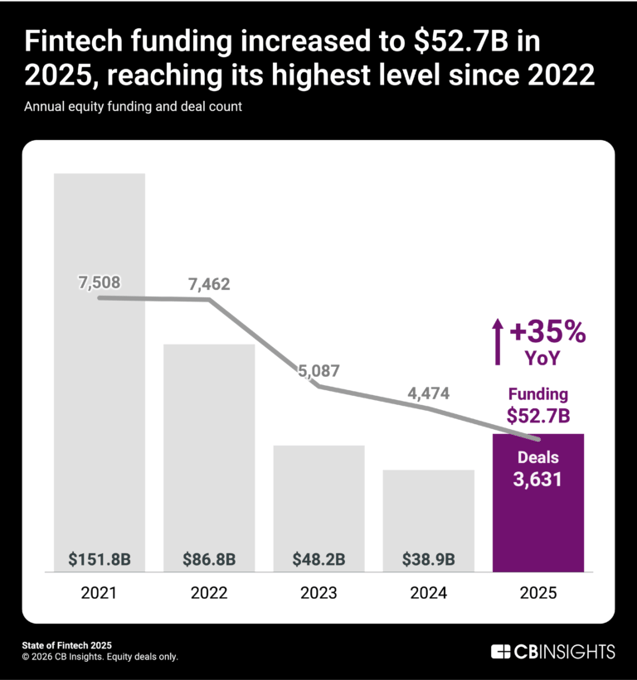

Fintech funding reached $52.7 billion in 2025 — its highest level since 2022 — with Q4 alone accounting for $16.4 billion, according to CB Insights' State of Fintech 2025 Report. AI-enabled fintechs captured 23% of Q3 2025 funding, the highest share since Q4 2023, with five of the 10 largest fintech deals going to companies heavily deploying AI.

PitchBook's Q4 2025 Venture Monitor confirms the trend: AI/ML deals captured 65.4% of all VC deal value in 2025 ($222 billion out of $339 billion), up from 49.1% in 2024. Within fintech, the concentration toward AI-powered infrastructure plays is accelerating.

That premium is justified — these companies are solving genuinely harder problems with stronger moats. The value creation is shifting from the front end to the foundation layer — data infrastructure, compliance automation, and payment rails.

More importantly, we've moved beyond "growth at all costs" toward sustainable, profitable growth. The companies that will define the next decade aren't the ones burning cash to acquire users — they're the ones embedding intelligence into existing platforms where users already are, creating value with better unit economics from day one.

Let's Connect

At Motley Fool Ventures, we're actively seeking Series A companies building in this space that meet our investment criteria:

- $1M+ in revenue with 100%+ year-over-year growth

- 50%+ gross margins

- Deep platform integration with measurable attachment rates and user engagement

- Demonstrable AI value with quantifiable improvements

- Diversified platform risk with a path to serving multiple host platforms or verticals

For Founders

If you're building an AI-powered embedded finance company and are close to meeting these criteria, I'd love to hear from you. Whether you're in early traction or approaching Series A, I'm particularly interested in connecting with founders who are:

- Embedding financial services into vertical SaaS platforms with 20%+ attachment rates

- Using AI to automate financial decisions with measurable accuracy improvements

- Building in B2B payments, lending infrastructure, or treasury management

- Developing proprietary data moats through platform integrations

For Investors

If you're a fellow investor with a differentiated take on where embedded finance is headed — whether you agree with this thesis or you have a different perspective — let's compare notes. I'm interested in hearing from investors who:

- Are seeing different metrics or benchmarks in embedded finance companies

- Hold contrarian views on AI's role in financial services

- Are tracking emerging competitors or business models I haven't considered

- Want to share deal flow in adjacent spaces where our theses might complement each other

Connect with me on LinkedIn.

The Foolish Bottom Line

The winners in fintech's next chapter won't build "fintech products with AI features." They'll build intelligent financial infrastructure that becomes indispensable to the platforms embedding it — creating compounding value through data network effects and continuous AI improvement.

This is infrastructure-level transformation, not feature innovation. The companies that understand this distinction — that are building the financial operating system for the next generation of software platforms — will capture disproportionate value. The question isn't whether AI-powered embedded finance will define the next decade of fintech — it's which companies will execute well enough to own it.